Financial Resolution of Partnership Disputes

Article 2: Partnership Accounting with Capital Accounts

By Serena Morones, CPA, ASA, ABV, CFE

Understanding the basics of capital accounts may be the most important take away from this series of articles. Capital accounts are a critical component in understanding a partner’s share of ownership of the partnership and yet for most professional advisors, they are the least understood aspect of a partnership. Before a partnership dispute is concluded, the capital accounts should be accurately calculated, reflecting the intended profit and capital sharing ratios of the partnership. The final capital account balance (or a hypothetical final balance) should indicate a partner’s final financial position (amount owed to the partner), not withstanding any side agreements relating to financial settlements.

Why are capital accounts so important to a partnership dispute resolution? Capital accounts are critical to a dispute resolution because according to RUPA Section 807(b), a partner is entitled to a distribution equal to his positive capital account balance upon dissolution of the partnership. A partner’s final capital account balance represents a particular partner’s share of the overall net assets, if the assets were to be distributed to all the partners. Therefore, a partner’s capital account balance has a direct bearing on the value of that partner’s interest in the partnership.

The Revised Uniform Partnership Act (RUPA) Section 401 sets out the rules for calculating capital accounts. RUPA section 807 sets out the rules regarding the settlement of the partners’ accounts upon the dissolution and windup. This form of accounting follows the aggregate theory of business ownership rather than an entity theory; a difference that becomes important when determining the value of a partner’s interest. Corporations do not utilize capital accounts.

The basic calculation of a partner’s capital account is as follows:

+ Initial capital contribution by Partner One

+ Plus Additional capital contributions by Partner One

+Plus Partner One’s share of profits

-Minus (Distributions to Partner One)

-Minus (Partner One’s share of losses)

———————————————————————–

= Partner One’s Capital Account Balance

Let’s review a simple hypothetical example to illustrate the use of capital accounts to determine a proper financial settlement in a partnership dispute.

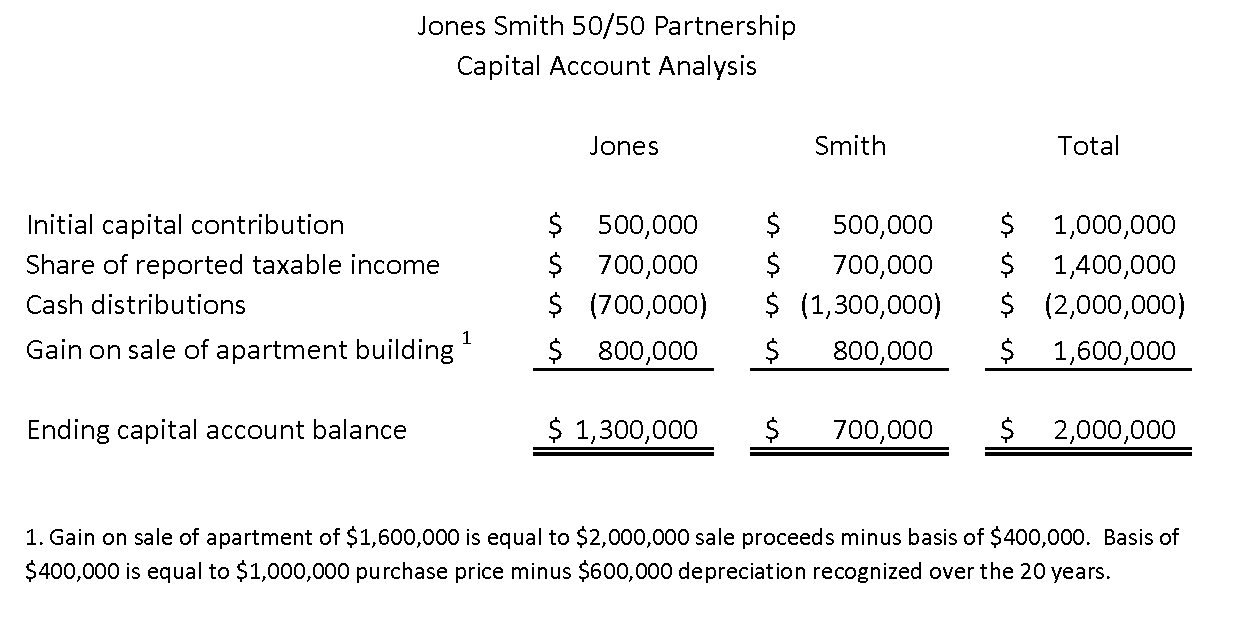

Jones Smith Partnership consists of two partners who decided to buy and operate an apartment building and share the profits 50/50. Jones and Smith equally contributed $500,000 to purchase an apartment for $1,000,000. Let’s assume they had no mortgage for the sake of simplicity. Smith volunteered to keep the books and bank accounts. Both partners agreed to participate in management.

Twenty years elapsed and the relationship between Jones and Smith slowly deteriorated over time. Jones could not seem to get Smith to disclose the accounting records after repeated requests. Jones received distribution payments every year but Jones believes there must be more money to distribute. Jones grew suspicious of Smith’s odd behavior, thinking that maybe Smith had taken money from the partnership. Fed up and wanting to move on, Jones hired an attorney to file a legal action to dissolve the partnership and compel payment to Jones of his share of partnership assets.

Assume the following additional facts:

- The apartment building was recently sold for net proceeds of $2,000,000

- Total taxable net income earned over the twenty years was equal to $1,400,000, not including income realized on the sale of the building.

- Cash distributions received by Jones over the twenty years was equal to $700,000

- Smith says there is very little cash left in the bank account.

- Jones does not know how much money in distributions Smith paid himself because he has not been able to examine the accounting records.

Jones knows that the amount received from the sale of the building was $2 million and he believes he should now receive 50% or $1,000,000. Jones also knows that over the twenty years he received distributions equal to 50% of the taxable income of $1.4 million or $700,000. On the surface, nothing looks wrong with Jones receiving $1 million in dissolution proceeds. But is a $1 million payment to Jones a fair financial resolution?

The answer is contained in the accounting records and calculation of the capital accounts.

Jones attorney files a lawsuit to dissolve the partnership and hires a CPA to conduct an accounting. The CPA discovers that like all income generating real estate partnerships, the partnership deducted substantial depreciation expense over the 20 years totaling $600,000. Depreciation expense does not result in a cash payment; therefore cash flow generated by the apartment building was $600,000 higher than taxable income. The CPA also discovers that there is no cash left in the partnership bank accounts. The CPA investigates further and discovered that Smith had deposited rent payments into his own personal bank accounts and used those funds to pay for other unrelated business and personal living expenses. The CPA concludes that Smith had constructively received $1.3 million in cash distributions while Jones has received $700,000.

Based on this additional information, what is the amount of money that should go to Jones and how much should go to Smith?

Here is the resulting capital account balances based on the above illustration:

Partners operating in a loose environment of a casually formed and operated partnership can fail to keep track of their respective financial positions. I have seen many partnerships where the partners failed to transact financial activity according to the intended agreement, and capital accounts fell out of balance compared to expectations. Out of balance capital accounts can result from partners paying non pro-rata distributions or make non pro-rata contributions or conducting other transactions that impact one partner’s capital account. I have seen situations where legal counsel assumed that a reasonable settlement would result from paying a pro-rata share of partnership asset value but did not realize that a partner’s capital account could be out of balance with respect to the agreed profit and capital sharing ratios, necessitating an equalizing adjustment.

Business Valuation

In our hypothetical example, let’s assume that a business appraiser is hired to determine the statutory fair value of Jones 50% interest in Jones Smith Partnership because Smith wants to buy-out Jones’ interest and not sell the apartment building. The appraiser is instructed not to consider discounts for lack of control or lack of marketability. Without inquiry into the status of the capital account balances, the business appraiser would likely conclude that Jones’ partnership interest is worth $1,000,000 because the adjusted net assets of the partnership is equal to $2,000,000. Business appraisers rely on assumptions provided to them, and many business appraisers are not CPAs with experience in partnership accounting. Attorneys involved in partnership disputes should be careful to select an appraiser who understands partnership accounting, or make sure that a qualified CPA with partnership experience communicates to the appraiser about the status of the capital accounts.

Limited Liability Companies

Limited liability companies (LLCs) also utilize capital accounts. LLCs offer great flexibility in the structuring of profit and capital sharing arrangements between members. Profit sharing ratios can differ from capital sharing ratios, including complex preferred return scenarios. And a member can have a profit interest without a capital interest. The accurate maintenance of capital accounts in an LLC is therefore even more critical because the extra flexibility afforded by LLCs also creates extra complexity when calculating one member’s share of total capital value upon dissolution.

I hope that these simple illustrations emphasize the importance of determining the final capital account balance of each partner before attempting to arrive at a fair financial settlement in a partnership dispute.

Please email me at [email protected] with any feedback or suggestions for topic areas that you think I should cover in this series.

Serena Morones, CPA, ASA, ABV, CFE

Read Article Three: Accounting for Partner Services

{kind=link}